It's been a while since I prepared a summary of the hospital industry in the Boston area. Some things have changed. Some remain the same.

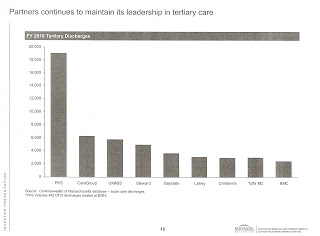

Partners Healthcare System (Massachusetts General Hospital, Brigham and Women's Hospital, Brigham and Women's Faulkner Hospital, Newton Wellesley Hospital, North Shore Medical Center, Martha's Vineyard Hospital, Nantucket Cottage Hospital, and more.) An expansion is in process with the pending acquisition of South Shore Hospital and Cooley-Dickinson Hospital. There are numerous clinical affiliations with other hospitals, also. PHS is doing very well, thanks to above market contracts signed with Blue Cross Blue Shield and other insurers. Do not ever expect to see above average earning reports, though, as the system is a master at burying its money in new buildings, information systems, and the like. Let there be no doubt that Partners has won the Massachusetts market for years to come. The rest of this post is about how the others will fight for the remaining scraps.

Partners Healthcare System (Massachusetts General Hospital, Brigham and Women's Hospital, Brigham and Women's Faulkner Hospital, Newton Wellesley Hospital, North Shore Medical Center, Martha's Vineyard Hospital, Nantucket Cottage Hospital, and more.) An expansion is in process with the pending acquisition of South Shore Hospital and Cooley-Dickinson Hospital. There are numerous clinical affiliations with other hospitals, also. PHS is doing very well, thanks to above market contracts signed with Blue Cross Blue Shield and other insurers. Do not ever expect to see above average earning reports, though, as the system is a master at burying its money in new buildings, information systems, and the like. Let there be no doubt that Partners has won the Massachusetts market for years to come. The rest of this post is about how the others will fight for the remaining scraps.

Steward Health Care System (St. Elizabeth's Medical Center, Carney Hospital, Good Samaritan Medical Center, St. Anne's Hospital, Holy Family Hospital, Merrimack Valley Hospital, Morton Hospital, Nashoba Valley Medical Center, Norwood Hospital, Quincy Medical Center, New England Sinai Hospital.) This is the big for-profit system, owned by private equity firm Cerberus, which acquired it from the former Caritas Christi system. Tongues were wagging recently when the Attorney General issued her first report on this system, showing operating losses in its first year of ownership.

For example, a colleague who studies municipal bonds said, "We are sitting here in tax-exempt bond land saying 'What was Cerberus thinking?' and 'How long are they going to stick it out, but on the other hand, what can they do, is somebody else going to buy them out at this point?' All very interesting, especially since the for-profit guys are so confident that they can play the game better. Perhaps not always."

Not so fast. Don't jump to conclusions. The report only covered operations for the year ending September 30, 2011. And remember that operating losses on the income statement are not the main concern for a private equity firm. Cash flow is what matters, earnings before depreciation and taxes. Depreciation is a non-cash expense. Taxes are subject to all kinds of IRS rules and loopholes.

Nonetheless, there are some things to watch. Recall that Steward has promised to be the low-cost alternative in the communities it serves. The AG found:

While 2011 prices were not available for this Report, 2009 and 2010 data shows that prices for the Caritas hospitals vary insurer by insurer, and by inpatient versus outpatient services, with the result that some Caritas hospitals are on par with competitors, others are less expensive, and others are more expensive. Given this variation in price by local market and service category, whether Steward’s activities will raise or lower costs in its markets ultimately depends on a variety of factors, from “endogenous” factors like the services Steward chooses to develop and the prices it seeks for those services, to factors “exogenous” to Steward, such as market activity by its competitors and changes in the regulatory landscape.

Steward has also been in the forefront of signing risk contracts with Blue Cross Blue Shield. Those contracts were front-end loaded to be made more attractive the health systems. Over time, their provisions will bind and can affect earnings. Even those provider groups with the most experience with risk contracts are now finding how difficult it is to generate surpluses. Does Steward have the care management system in place to be successful under this payment scheme? How does it control the costs of tertiary referrals now that St. Elizabeth's really isn't a high-end hospital and when its main clinical partner for those referrals is MGH?

Personnel changes in recent months might be indicative of cultural problems or concerns about specific hospital business plans. Highly regarded Bill Walczak, the former head of the Codman Square Health Center, was hired to be CEO of Carney Hospital but then was quickly fired. More recently, well respected John Polanowicz left the helm of St. Elizabeth's to join the state government less than two years after signing on. There are rumors, too, that the system's consolidated hospital billing system has had start-up problems. Effective operational management is necessary even for a system that plans to do a flip in a few years.

Beth Israel Deaconess Medical Center (BIDMC, BID Hospital~Needham, Milton Hospital.) After the recent merger with Milton Hospital, an expansion continues with the acquisition of Jordan Hospital. It maintains clinical affiliations with several other hospitals, including the two other Caregroup hospitals, Mt. Auburn Hospital and New England Baptist Hospital. BIDMC is apparently engaged in a strategy of acquisitions to provide a tighter network in the world of Accountable Care Organizations. Are others in the offing? While this strategy is understandable, the challenge will be how to integrate the governance and operations of a system of hospitals, as contrasted with what has essentially been a lone academic medical center with one small community hospital outpost. The governance and operation of a health system require a different set of skills and approaches. (Of course, I am loyally rooting for success!)

Tufts Medical Center. I'm sorry to report that I haven't heard anything about the smallest of the academic medical centers, except the loss of Jordan Hospital as a referral source. The hospital has had and continues to have thoughtful and excellent leadership, but it is not clear where their strategic path is to a happy future. I'm hoping I just don't have the wisdom to see the path, as this is a treasured Boston institution, going back to 1796: "A group of public-spirited Bostonians founded the Boston Dispensary, funding tickets that enabled the city's poor to receive treatment. One of the original tickets was signed by subscriber Paul Revere." Hmm, maybe there is a deal to be done with BIDMC?

Switzerland. Places that have some geographic advantage like Southcoast Health System (owner St. Luke's Hospital in New Bedford, Tobey Hospital in Wareham, and Charlton Hospital in Fall River) seek to maintain independence and offer affiliations with all the others. As noted by the Boston Business Journal: "Southcoast Health System is strengthening its clinical offerings and financial position as it strives to endure as an independent community health care system, with no ties to a Boston academic medical center or an out-of-state company."

Steward Health Care System (St. Elizabeth's Medical Center, Carney Hospital, Good Samaritan Medical Center, St. Anne's Hospital, Holy Family Hospital, Merrimack Valley Hospital, Morton Hospital, Nashoba Valley Medical Center, Norwood Hospital, Quincy Medical Center, New England Sinai Hospital.) This is the big for-profit system, owned by private equity firm Cerberus, which acquired it from the former Caritas Christi system. Tongues were wagging recently when the Attorney General issued her first report on this system, showing operating losses in its first year of ownership.

For example, a colleague who studies municipal bonds said, "We are sitting here in tax-exempt bond land saying 'What was Cerberus thinking?' and 'How long are they going to stick it out, but on the other hand, what can they do, is somebody else going to buy them out at this point?' All very interesting, especially since the for-profit guys are so confident that they can play the game better. Perhaps not always."

Not so fast. Don't jump to conclusions. The report only covered operations for the year ending September 30, 2011. And remember that operating losses on the income statement are not the main concern for a private equity firm. Cash flow is what matters, earnings before depreciation and taxes. Depreciation is a non-cash expense. Taxes are subject to all kinds of IRS rules and loopholes.

Nonetheless, there are some things to watch. Recall that Steward has promised to be the low-cost alternative in the communities it serves. The AG found:

While 2011 prices were not available for this Report, 2009 and 2010 data shows that prices for the Caritas hospitals vary insurer by insurer, and by inpatient versus outpatient services, with the result that some Caritas hospitals are on par with competitors, others are less expensive, and others are more expensive. Given this variation in price by local market and service category, whether Steward’s activities will raise or lower costs in its markets ultimately depends on a variety of factors, from “endogenous” factors like the services Steward chooses to develop and the prices it seeks for those services, to factors “exogenous” to Steward, such as market activity by its competitors and changes in the regulatory landscape.

Steward has also been in the forefront of signing risk contracts with Blue Cross Blue Shield. Those contracts were front-end loaded to be made more attractive the health systems. Over time, their provisions will bind and can affect earnings. Even those provider groups with the most experience with risk contracts are now finding how difficult it is to generate surpluses. Does Steward have the care management system in place to be successful under this payment scheme? How does it control the costs of tertiary referrals now that St. Elizabeth's really isn't a high-end hospital and when its main clinical partner for those referrals is MGH?

Personnel changes in recent months might be indicative of cultural problems or concerns about specific hospital business plans. Highly regarded Bill Walczak, the former head of the Codman Square Health Center, was hired to be CEO of Carney Hospital but then was quickly fired. More recently, well respected John Polanowicz left the helm of St. Elizabeth's to join the state government less than two years after signing on. There are rumors, too, that the system's consolidated hospital billing system has had start-up problems. Effective operational management is necessary even for a system that plans to do a flip in a few years.

Beth Israel Deaconess Medical Center (BIDMC, BID Hospital~Needham, Milton Hospital.) After the recent merger with Milton Hospital, an expansion continues with the acquisition of Jordan Hospital. It maintains clinical affiliations with several other hospitals, including the two other Caregroup hospitals, Mt. Auburn Hospital and New England Baptist Hospital. BIDMC is apparently engaged in a strategy of acquisitions to provide a tighter network in the world of Accountable Care Organizations. Are others in the offing? While this strategy is understandable, the challenge will be how to integrate the governance and operations of a system of hospitals, as contrasted with what has essentially been a lone academic medical center with one small community hospital outpost. The governance and operation of a health system require a different set of skills and approaches. (Of course, I am loyally rooting for success!)

Tufts Medical Center. I'm sorry to report that I haven't heard anything about the smallest of the academic medical centers, except the loss of Jordan Hospital as a referral source. The hospital has had and continues to have thoughtful and excellent leadership, but it is not clear where their strategic path is to a happy future. I'm hoping I just don't have the wisdom to see the path, as this is a treasured Boston institution, going back to 1796: "A group of public-spirited Bostonians founded the Boston Dispensary, funding tickets that enabled the city's poor to receive treatment. One of the original tickets was signed by subscriber Paul Revere." Hmm, maybe there is a deal to be done with BIDMC?

Switzerland. Places that have some geographic advantage like Southcoast Health System (owner St. Luke's Hospital in New Bedford, Tobey Hospital in Wareham, and Charlton Hospital in Fall River) seek to maintain independence and offer affiliations with all the others. As noted by the Boston Business Journal: "Southcoast Health System is strengthening its clinical offerings and financial position as it strives to endure as an independent community health care system, with no ties to a Boston academic medical center or an out-of-state company."

21 comments:

How about a few comments on Boston Medical Center?

A wonderful place with great people and a special mission, as the main safety net hospital for Boston. Unlikely to find a suitor because, rightly or wrongly, it is viewed as unmanageable with 14 unions.

Your insight on the challenges of ACOs is spot on. Many, many people think insurance is easy; they often talk of profit sharing. It is RISK sharing, and not easy. There is enough energy, money and incentive to get it figured out but there will be rough patches and not all will make it.

...and let us not forget Camelot, otherwise known as Landmark Medical Center, just over the line, but well in reach of referrals north, and southeast!

I was wondering if there is any available information that would get at differences in costs among these systems. I would be particularly interested in data showing the number of employees per licensed bed for each system’s academic medical centers, if any, and their community hospitals. Also, to what extent are there differences in the mix between inpatient surgical and medical bed days and outpatient revenue as a percentage of total revenue?

Separately, what’s happening in Massachusetts regarding price transparency, especially for hospital based care? My understanding is that the Healthcare Quality and Cost Council has much of this data and could release it if it wants to. Where is it?

Paul - Right on about Partners basically owning the Massachusetts marketplace. They should NOT be allowed to add South Shore Hospital to their network contracts as they are already a monopoly that sets the cost of healthcare in their service area. The local Medicare ACOs are already complaining to the Feds because they lost money in 2012 and the BCBS AQC contract will generate money via the quality component... not the risk side. Steward is going to have a tough time finding a buyer as they have all of these empty hospitals that keep losing money. The Globe article this weekend raised the correct question asking about the $100 million generated from the sale of the Steward Medical Office Buildings.... did Cerberus take a dividend payment of that money in 2012? The article said they didn't file anything but that was not a final answer... did they or didn't they extract cash out of Steward in 2012 that went to Cerberus in New York? I would guess they did before the most recent federal tax hikes. You didn't really touch on it but the other for profit Vanguard is tied in with NEMC and have a for profit joint venture. You also didn't mention the other monopoly over at Children's where they have gobbled up all of the PCP practices of Pediatricians in their network and have total market domination and bury their profit margins just like Partners does. Lots going on.

Your comments about BID and Tufts Medical Center "TMC" intrigue me and make much sense.

They have much overlap in what they are doing. Both have relationships with Jordan, Southcoast, Vanguard (metrowest and St Vincents), Signature (Brockton hospital), Lawrence General, Winchester hospital and others...

TMC also had a historical relationship with Milton, and has an ongoing relationship with Cambridge Health Alliance which is an alliance target for BID.

A partnership between BID and Tufts that included the above hospitals and could act on Vanguard's desire to grow its chain and TMC's historical relationship with the Caritas hospitals would be formidable....

Barry,

All those numbers and more are in the all claims all payer data base collected by the state. To date, they have not seen the light of day.

Paul,

I thought both the Patrick Administration and the Massachusetts state legislature have a keen interest in trying to mitigate healthcare cost growth especially now that near universal health insurance coverage has been achieved in the state. It’s extremely disappointing that information that could help both referring doctors and patients make more intelligent and cost-effective care choices is being withheld from the public. Is it the providers or the payers or both that continue to lobby to withhold the release of the information in the all payer all claims database? Maybe the Boston Globe should write about this if it hasn’t already.

when the cost hearings were held ending a little over a year ago, including some of the attorney generals analysis, some of that information was included. The general information was covered, though more details were available.

Looked into quality, cost, social security case mixes, inpatient and outpatient volumes, financial status of patients treated and more. Said the most expensive hospitals like MGH and B&W, have much higher prices than hospitals like TMC, which was the lowest cost, but quality was no different.

When the nurses threatened to strike hospitals like Metrowest, TMC etc, a year ago they talked about lower nursing staff levels at hospitals like TMC.

TMC responded and provided data, which showed that while their nurse staffing levels were lower, they reduced the amount of "scut work" done by nurses and higher more orderlies and lesser paid technicians to do it. They showed data proving their quality went up as their staffing went down. And again, the attorney general and cost commission showed that lower paid AMC had similar quality to the highest paid.

We must be careful about using resources as a proxy for quality, because resources including personnel are often not used well.

In a world were the US spends, 18% of GDP on health care while the rest of the industrialed world spends 12% of less, and we don't have universal coverage, and in some was lesser quality (bad preventive care compared to most of the rich world), there are certainly many things we can do to improve care.

Paul has long been an advocate of three sigmas which came from industry. Toyota one of the most avid early users of Demings techniques had higher quality and lower costs for many years.

If just look at things like resources and not outcomes it always looks like a MGH, or a GM is better when in fact they are not.

Barry,

The all claims all payer database used to be in the hands of DHCFA, a line state agency that was subject to political pressure from the governor's office.

Now it is in the hands of the Center for Health Information and Analysis (CHIA), an independent agency. It will be interesting to see if they have the guts to make the data more widely available.

Here's more description:

"The Center for Health Information and Analysis (CHIA) is established by the historic health care cost containment legislation that the Governor signed on August 6, as the successor agency to the Division of Health Care Finance and Policy. CHIA is an independent state agency that collects health care cost and quality information and provides objective analysis of this data to assist in the formulation of health care policy. CHIA maintains a number of the Division’s responsibilities, including the compiling of the state’s annual cost trends reports, managing the state health data repository, and monitoring the financial stability of hospitals and health plans. CHIA also maintains a consumer health information website to enhance the transparency of the quality and cost of health care services in the Commonwealth.

"CHIA is led by an Executive Director. The Executive Director is chosen by a majority vote of the Governor, the Attorney General and the State Auditor for a term of 5 years. Chapter 224 will be effective on November 5, 2012."

From: http://commonhealth.wbur.org/2012/11/aron-boros-named-director-of-new-center-to-implement-cost-control-law

Do you have any insights about the Lahey acquisition of Northeast?

Anonymous 2/5/2013@9:38 A.M.,

I’m interested in the number of employees per licensed bed as a proxy for cost, not for quality. I’m told that 60% of a typical hospital’s cost is attributable to employee wages and benefits. Perhaps total compensation per licensed bed would also get at how efficiently resources are used as well which would include using lower paid people when they can competently perform tasks that higher paid people do in less efficient, higher cost hospitals.

Sorry I misunderstood about looking at resources to evaluate quality vs cost. I was concerned because looking at resources utilized as a proxy for quality is something done by unions to "feather bed" and as justification for higher prices and profits by groups that don't typically compete based on price like hospitals/medical care/defense contractors etc....

If the objective is a to look at "bloat" typically what is done is bench marking. Find an institution that produces the outcomes you want a lower cost and learn what they are doing right by looking at things like (as you suggest):

1) resources used per bed

2) support staff per doctor

3) support staff per nurse

4) levels bureaucracy between front line workers and senior management

etc...

Bench marking against the best performers will answer your questions. But the Best are not likely to be in the USA. (See Pauls posting of Jan 21, 2013 on Israeli cost for health care). Most of the countries we like to compare ourselves with spent between 10% and 12% in 2010 vs our 18%. So the best hospital performers are likely to be somewhere outside the US. For something more local, Dartmouth studies showing regional differences in the US health care spending based on Medicare data, might be a place to start. Find the best performing medical centers in the US and benchmark.

By the way....for our healthcare system...for places were accountable care organizations are up and working......one good approach would be looking at

-- "things" per general practitioner

resources

costs

etc...

that would help show too many, overpriced specialists, too much duplication of testing, too many drugs that have marginal (if any) improvements in efficacy at huge increases in cost....etc etc...

I’ve said on several occasions that I would love to see a study that compared the number of employees per licensed bed between U.S. community hospitals and academic medical centers vs. similar hospitals in other developed countries. I’ve never seen one. The health economist, Uwe Reinhardt, a professor at Princeton, says that such a study would be complex and expensive to do though I don’t understand why. At any rate, CMS should be easily able to afford to finance it. Alternatively, perhaps a foundation like Robert Wood Johnson or Bill and Melinda Gates would like to take it on.

If such a study could be done making both international cost comparisons as well as comparisons just among U.S. hospitals, I’ll bet the results would be insightful. The labor intensity of U.S. hospitals should be somewhat higher due to more complex billing. Also, I’m told that functions like credentialing of physicians are done at the state level in Germany, like issuing drivers licenses in the U.S., but at the hospital level in the U.S. There could also be regulation driven differences in areas like nurse staffing ratios while the recent trend toward more private hospital rooms would suggest higher maintenance costs in the U.S. That all said it would be instructive to highlight just where the inefficiencies are which would make it easier to target corrective action.

Thanks for the thoughtful updates, this is one of my favorite aspects of your blog.

The M&A activity across the country seems frantic when compared to my area - the greater Philadelphia region. Sure, Fox Chase and Temple merged, Southern NJ Hospitals are talking about merging in various forms, and Penn and Chester County are going together... but it still seems rather tame compared to the Boston market.

The results of international benchmarking would enrage many in the medical community.

It would show massive waste and in many cases much higher salaries for essentially the same work as is done for much less in other developed countries with standards of living in the same range as ours. As someone said earlier most of the cost in medicine is salaries to someone. We essentially pay too many people too much with much waste mixed in.

Steward Health Care CFO James Renna leaving to take a job at a Boston Private Equity firm per press release. Wonder if anything else is driving the senior management leaving Steward as St. Elizabeth's just lost their CEO as well??

This is an absolutely fantastic blog and your insights are quite fascinating. I'm trying to learn more about local market dynamics, as someone about to start practice, and your thoughts are required reading...

Paul:

Excellen insightful posts....the departure of James Renna is likely a harbinger of economic turmoil...any updates on Stewards financial stability??

Post a Comment